> Most crypto founders design tokens like meme stocks and then wonder why the price won’t hold. Design the token as the router for every major cashflow in your business, and price becomes a byproduct of a system that actually works.

Most founders join a tokenomics call with a single goal: “How do we make the token go up?” That’s the wrong brief. Price is an output, not a design variable.

The real question is: how do we route this business’s cashflows through a token so that users, contributors, and investors all get paid in the right order, with the right risk?

Protocols like GMX and Maker didn’t win because they drew cleaner emission curves. They won because they wired their business model directly into on-chain cashflows.

In this post, we’ll unpack what “token as cashflow router” actually means, why treating the token like equity quietly kills protocols, and how to translate your own business model into a structure that can sustain a token over a 5–10 year horizon.

“Token price go up” is the wrong design question

When founders fixate on “number go up,” they end up treating the token like a meme stock. The whole design debate narrows to emissions, buybacks, and launch price. That’s upside down.

In every resilient protocol, token price is a lagging reflection of whether the underlying system is routing value correctly. If your token has no direct claim on protocol cash flows, no essential role in the core user journey, and no mechanism to balance winners and losers over time, no vesting schedule on earth will bail you out.

The right first question is: what are the actual economic flows in this business — fees, spreads, interest, ad revenue, sponsorships — and who should be paid, in what order, and under which conditions?

Once you can sketch that cleanly on a whiteboard, tokenomics stops being vibes and starts being engineering.

Design the token as a cashflow router, not an equity clone

Treat your token as a programmable router for value and risk, not a one-to-one equity clone.

Equity is a blunt instrument: a residual claim on whatever’s left after everyone else in the stack gets paid. Tokens don’t have to be that coarse. They can be precise, conditional, and composable.

A token can:

- Route specific fees to specific stakeholder groups

- Change routing rules dynamically based on on-chain behavior or system state

- Spin up new cashflow pipelines as new products and markets come online

GMX is a straightforward illustration. Traders pay fees. Those fees are programmatically split between GLP liquidity providers and GMX stakers. The GMX token is wired into that logic layer; it’s the object that encodes who gets what, when, and under which conditions.

Maker followed a similar pattern. Early on, MKR governed DAI stability fees. Over time, Maker extended that into real-world asset vaults, where on-chain fee flows and risk parameters are ultimately controlled by MKR holders. Again, the token is embedded directly into the system’s economic routing rules.

In both architectures, the token is not “equity, but on-chain.” It is the switchboard that determines how every incremental unit of value is allocated as it moves through the protocol.

!Flow of a dollar of protocol revenue through a token as a cashflow router

{kind=link}

This is what you should be designing: a clear, machine-readable map of how each dollar of value is split between treasury, risk buffers, and the people who make the system work.

GMX, Maker, and the graveyard of failed launches

Look at GMX and Maker versus the long tail of 2021 launches that vanished. A lot of those protocols cloned emissions charts and headline APYs, but never plugged the token into the core machinery of the business. Fees funneled into a team multisig instead of back to token holders. Governance was theater. The token behaved like a speculation coupon, not a router for fees and value.

Once volumes fell, there was nothing structurally binding the system together, so it just unwound. GMX, on the other hand, could cut emissions and still retain stakers because real trading fees were being pushed through the token. Maker made it through multiple bear cycles because MKR holders had direct control over DAI stability fees and collateral onboarding — the cashflows and risk knobs that actually matter.

The takeaway is blunt: if your token goes to zero and the product keeps running just fine, you didn’t build a cashflow router; you printed a scratch-off lottery ticket.

How to map your business model into on-chain cashflows

Begin with a ruthlessly clear P&L for your protocol. Map every dollar in and every dollar out.

Where does revenue actually come from — trading fees, interest spreads, SaaS subscriptions, NFT mints, sponsorships, something else? Where does it go — infrastructure, team, partners, insurance, reserves, buybacks, liquidity? Put hard numbers against each line, even if they’re rough, and make your assumptions explicit.

Then ask two questions for every line item:

- Should this flow live on-chain?

- Should the token have any claim on it?

For every stream the token does touch, define the rule set with precision:

- What percentage goes where?

- Which stakeholders receive what?

- Under which conditions?

- Can governance change it, and if so, how?

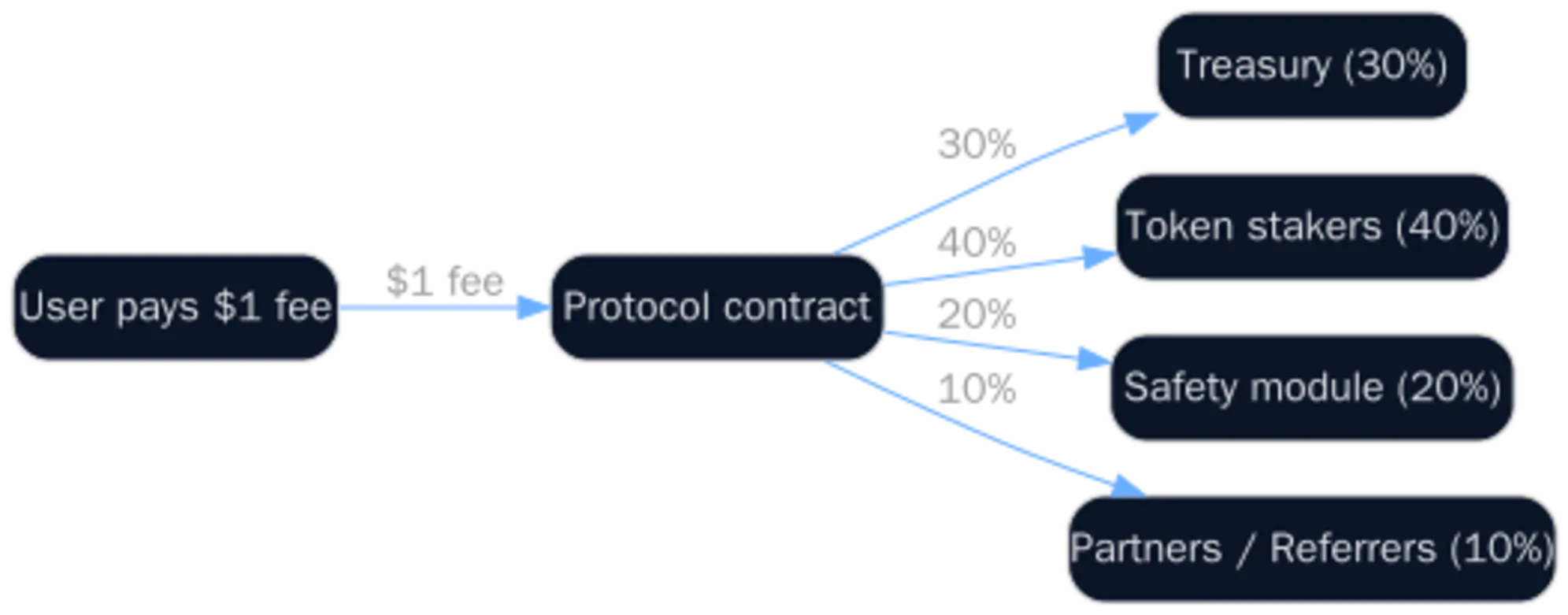

Turn that into a simple, machine-readable flow:

- User pays X into the protocol

- Smart contract automatically routes: Y% to treasury, Z% to stakers, W% to a safety module, etc.

Only once this routing logic is nailed down do you design supply, emissions, lockups, and incentives around it. Those token mechanics exist to strengthen the economic circuit you’ve already defined — not to substitute for it.

The token’s core function is to make these cash-flow rules:

- Credible (enforced by code and process)

- Transparent (observable and auditable on-chain)

- Difficult to be altered quietly (protected by clear, robust governance paths)

A pre-flight checklist before you hire tokenomics help

Before you bring in a tokenomics advisor, you should already have five answers locked in.

First: if all emissions stopped tomorrow, what real, hard cashflows would still interact with this token?

Second: who are the three core stakeholder groups, and exactly which cashflows do each of them actually care about?

Third: can you sketch, on a single page, how one incoming dollar gets split across those groups?

Fourth: under what conditions would that split change, and who has the authority to make that call?

Fifth: if the token went to zero, would your product still operate the same way?

If the honest answer to the last one is yes, you’re not facing a token design issue; you’re facing a business model issue.

Walk into an advisor meeting with these answers and a rough flow diagram, and you’ll get engineering-grade thinking instead of another glossy deck full of buzzwords and pretty curves.

Key takeaways

- Token price is a lagging indicator; design the cashflow router first, then worry about valuation.

- Durable protocols wire every major cashflow through the token with explicit, on-chain rules.

- If your product works fine without the token, you’ve built a lottery ticket, not an economic engine.

- Start tokenomics with a brutally honest P&L and a one-page flow of how each dollar is split.

- Show up to advisors with clear cashflow maps and constraints if you want real engineering, not vibes.

Frequently asked questions

How do I know if my token actually has a claim on cashflows?

Ask a simple question: when the protocol earns $1 of revenue, does any part of that dollar have to touch the token contract or token holders? If the answer is no, or it only happens via discretionary team decisions, your token doesn’t have a real claim.

Can I retrofit cashflow routing into an existing token?

Yes, but it’s harder. You’ll need to introduce new contracts or modules that redirect fees, and then pass governance proposals to wire those flows to token holders or staking contracts. Expect pushback if you’re changing expectations for existing holders.

What if my business model doesn’t generate fees yet?

Then your priority is to validate a real revenue model before you launch a token. You can still experiment with points or off-chain rewards, but don’t harden a token design around hypothetical cashflows that don’t exist.

How many cashflow streams should a token touch at launch?

For most early protocols, one to three clear, well-defined streams are enough. Too many routes at launch create confusion and make it harder to reason about risk and value capture.

Do I need complex bonding curves or exotic mechanics to make this work?

No. Most successful protocols use relatively simple routing rules: fixed fee splits, straightforward staking rewards, and clear governance over changes. Complexity should come later, only if it solves a real problem.

Need help with a blockchain project?

Applicature has been building blockchain solutions since 2017. Talk to our experts.

Get a Free Consultation